Deposits are shifting. What’s driving it and what banks do next

Deposit migration is visible in transaction data. KlariVis’ February 2026 study examines customer-initiated transfers between US community banks and Coinbase across Dec 2024 to Dec 2025, treating those transfers as a practical indicator of how easily balances can move onto digital rails. In the subset where transaction directionality could be determined, net flows skew outward over the observed period.

Architectures for Tokenized Deposits: Three Paths, One Core Question

Banks are exploring tokenized deposits because today’s payment infrastructure has hit clear limits. Money still doesn’t move across institutions with real-time finality, programmability, 24/7 availability, or smooth interoperability with digital assets.

Tokenization isn’t about creating a new type of money. It’s about giving existing deposits the ability to move instantly, reduce reconciliation work, automate financial flows, and operate beyond traditional banking hours – all while staying within familiar regulatory frameworks.

What Real-World Cases Reveal About Stablecoins and Tokenized Deposits

The debate over the future shape of digital money often remains abstract. Concepts like “programmability,” “fractional reserves,” or “public blockchains” appear detached from the day-to-day realities of banking and finance. Yet over the past years, real events — from stablecoin volatility to large-bank failures, from permissioned pilots to public-market stress — have provided a concrete laboratory for understanding what different forms of digital money can and cannot safely do.

AI vs Blockchain. Who Runs the Future of Banking?

As the fintech conversation evolves, two narratives are shaping the future of finance: the modernization of financial infrastructure through tokenization — and the rapid rise of artificial intelligence.

For now, they are moving in parallel. One is redefining how money moves, the other — how decisions are made.

Stablecoins Are Changing the Game. Are Banks Ready?

The financial sector is no longer competing only with FinTech apps or digital UX solutions. The real challenge lies deeper — in the architecture of money itself. Stablecoins are proving that speed and liquidity can move outside banks. The question is: how can institutions combine this with trust, compliance, and governance?

Stellar on DCM: Transparent Network and the Future of Banking Infrastructure

On September 29, Stellar shared a case study about DCM — highlighting how Ukrainian banks are pioneering a new model of payments. We’re grateful for this recognition, and want to add further context: facts that reveal how this story began, how it works in practice, and what it means for the future of banking infrastructure.

Welcoming Nick Tomadakis as Chief Product & Growth Officer at DCM

We’re thrilled to introduce Nick Tomadakis as our Chief Product & Growth Officer at DCM.

Nick brings over two decades of banking leadership across Barclays, Visa, Revolut, and Rakuten Viber — building everything from digital KYC to scaled global wallets. He’s led teams through market shifts, regulatory challenges, and product breakthroughs — always with a laser focus on simplicity, user value, and high-performance culture.

Overcoming Travel Rule Challenges in Blockchain Protocols: Impacts on Stablecoin Development and DCM’s ISO 20022 Solutions

The Travel Rule, mandated by the Financial Action Task Force (FATF), requires Virtual Asset Service Providers (VASPs) to exchange customer information during transactions exceeding certain thresholds to combat money laundering and terrorism financing.

Transforming Instant P2P Payments: DCM’s Alias and Processing System

In today’s rapidly evolving payment landscape, seamless payment experiences can make or break a bank’s competitive edge. At DCM, we’re excited to showcase our latest breakthrough: a P2P transfer alias system that lets users send money using just a phone number and connects different banks.

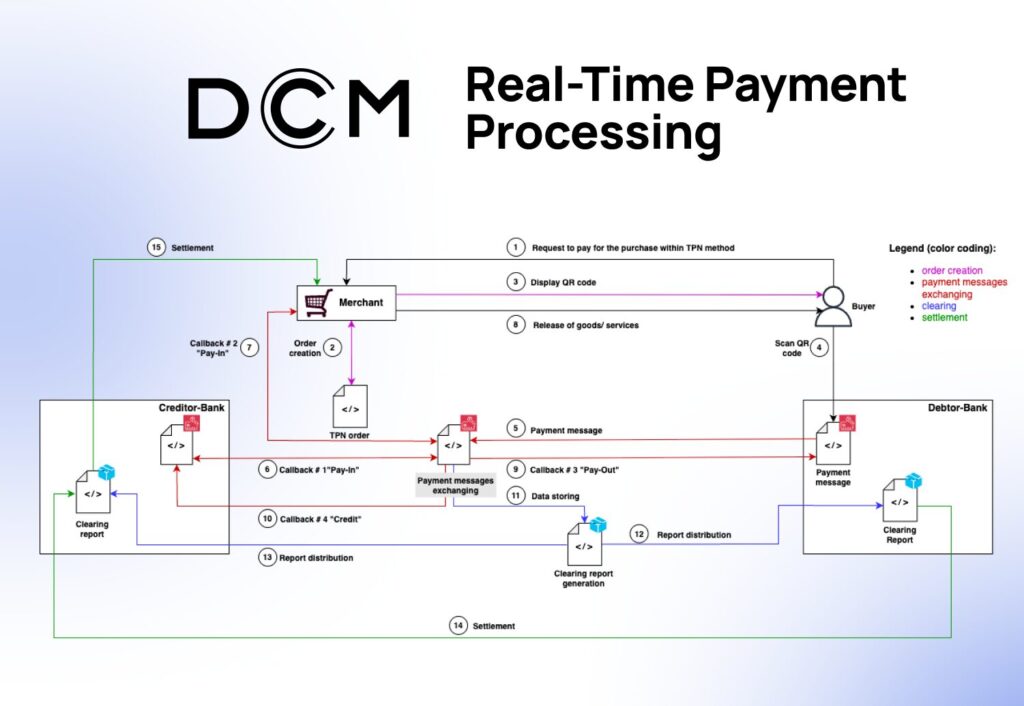

Real-Time Payment Processing: A Complete Transaction Journey

Before exploring how DCM software facilitates seamless payment flows, it’s essential to comprehend the intricacies of modern payment ecosystems. Every transaction involves multiple stakeholders, including buyers, merchants, banks, clearinghouses, and payment processors. Each step in this chain traditionally required separate communications, reconciliations, and time-consuming settlement processes.

How DCM Powered the Success of Transparent Network

At DCM, we believe that powerful technology should be intuitive, reliable, and designed for scale. We’re proud to be the tech provider behind Transparent Network, a consortium of banks that provides a next-generation instant account-to-account payment service. Transparent Network banks recently delivered impressive results in a promo campaign.

DCM TRACE: The New Standard for Financial Transparency and Control

Modern financial technologies are revolutionizing how governments and international organizations manage money.

DCM: Redefining Security for Modern Financial Transactions

Keeping financial transactions secure in our fast-moving digital world. We at DCM are committed to safeguarding your data and payments with a powerful and transparent security system. Designed to protect everything from interbank transfers to everyday payment processing, our solution sets a new standard for trust and reliability. Let’s explore how DCM keeps your transactions safe and sound.

Unlock Fast Blockchain Integration for Your Bank or Fintech: Simple, Secure, and Cost-Effective

In today’s fast-paced financial landscape, banks and fintech companies are under increasing pressure to optimize processes and develop innovative products that meet the demands of modern consumers. However, integrating traditional banking systems with advanced technologies like blockchain often presents significant challenges. High costs, complexity, and the need to ensure compliance with stringent regulatory standards can make this transformation seem daunting.

The Future of Stablecoins: Will Tokenized Bank Deposits replace them?

Stablecoins have become a cornerstone of the cryptocurrency ecosystem, bridging the gap between volatile digital assets and the stability of traditional fiat currencies. However, as financial technology evolves, alternatives like tokenized bank deposits and central bank digital currencies (CBDCs) are gaining traction. Could these innovations eventually make stablecoins obsolete? Or will they coexist, each serving distinct purposes in the global financial system?

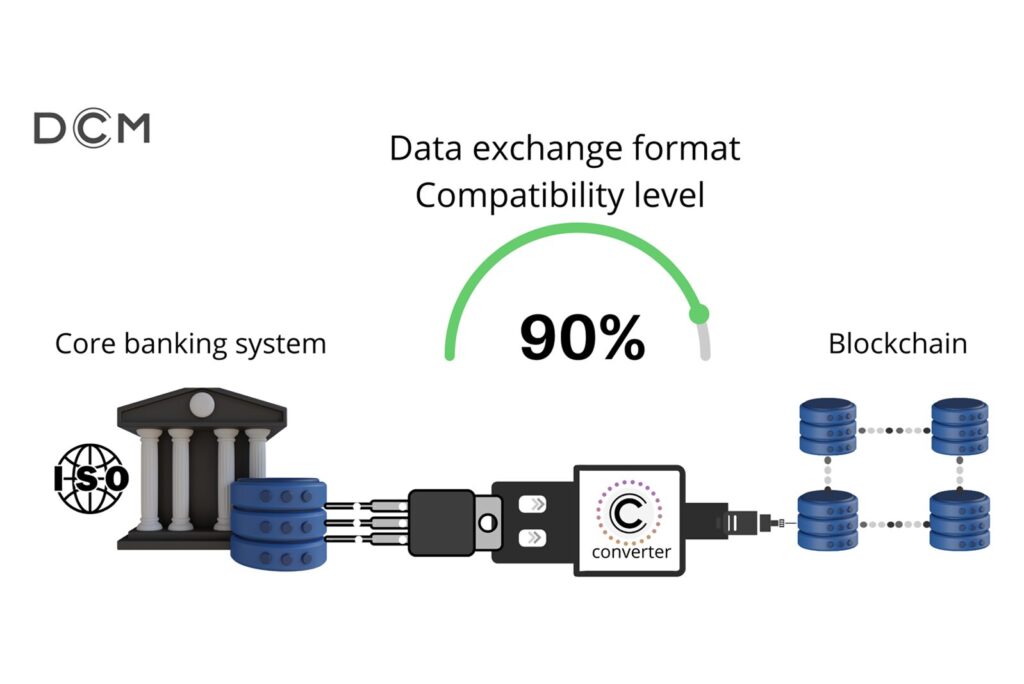

Bridging the Gap: How ISO 20022 is Paving the Way for Blockchain in Finance

As the world of finance rapidly evolves, a standardized approach to data exchange is essential to improve communication, reduce errors, and simplify transactions. Enter ISO 20022, a global messaging standard becoming necessary in the banking sector. This standard is reshaping traditional finance and setting the stage for blockchain interoperability. Adopting ISO 20022 is a critical step for blockchain networks to interact effectively with global financial systems.

DCM’s Clearing & Settlement Solution: A Comprehensive, Secure System for Financial Institutions

DCM’s Clearing and Settlement software offers a seamless, secure, and transparent solution for managing financial obligations. It utilizes blockchain technology and supports the ISO 20022 standard for enhanced interoperability. By leveraging advanced technology and aligning with

Payment Message Processing (PMP) in DCM: Ground-breaking Payment Solution with Blockchain Interoperability

In the rapidly evolving world of digital payments, seamless, secure, and cost-effective transactions are paramount. Payment Message Processing (PMP) within the DCM platform emerges as a game-changer, offering an innovative solution for the instant exchange of payment messages between financial institutions, businesses, and customers. This powerful feature simplifies the payment process and enhances decision-making and operational efficiency for all parties involved.

ISO 20022 and Blockchain Interoperability for Banks

The financial industry is undergoing rapid transformation with the emergence of new technologies like Distributed Ledger Technology (DLT) and the widespread adoption of ISO 20022, a standardized messaging framework for financial transactions. As these innovations gain traction, the question of interoperability between ISO 20022 and DLT becomes increasingly essential.

The launch of Transparent Network in Ukraine

This is one of the most progressive retail payment and transfer projects, implemented considering the global experience and the latest technologies, ensuring reliability, speed, and cost-effectiveness. The creation of the Transparent Network, initiated by the Independent Association of Banks of Ukraine (NABU), is supported by the banking community, Ukrainian businesses, and international partners.

The Shifting Payment Landscape: Rising Demand for Programmable Payments

Automation is now at the peak of popularity, with every business process using it to some degree. For example, we can see a high level of automation in customer support, task management, goods delivery, reporting, and more.

Payment Security and Transparency: Friends or Enemies?

With the development of digital payments, payment fraud is also growing. Payment fraud poses a serious threat to businesses because it allows attackers to use stolen or fake payment information to steal user funds. According to a recent Ravelin report, 75% of companies confirm that fraud affects their business. Additionally, for over 27% of organizations, fraud costs more than $15 million every year.

Top 10 Benefits of Instant Mass Payments for Banks

Categories Top 10 Benefits of Instant Mass Payments for Banks All, Insights Large companies, e-commerce platforms, and financial institutions often need to process numerous payments quickly. Processing each payment individually is highly time-consuming and inefficient. This increases the risk of payment delays, potentially leading to dissatisfied customers and harming the business’s reputation. Luckily, mass payments, also called batch or bulk payments, solve this problem. They offer a simple way to process large numbers of transactions simultaneously. What are batch payments, and how can organizations benefit from using them? This post will provide an explanation. What are mass payments? Mass payments are instant electronic transfers of any amount to multiple bank accounts opened by individuals. The payer decides how many accounts to send money to using mass payments. The key point is that there should be more than one account. What bulk payments are is sending payments to several recipients simultaneously. What bulk payments are not is sending payments to each recipient one by one. Batch payments may include: Paying salaries to company employees. Distributing dividends to shareholders. Making bulk e-commerce payments. Online mass payments are usually made through a special mass payment platform and conducted in any currency. Mass payments significantly simplify a company’s interaction with its clients and partners. They allow businesses to quickly and reliably make regular payments in batches. When businesses need mass payment solutions Businesses need mass payment solutions when they face the need to make many payments at the moment. Here are specific cases when mass payments are needed: Payrolls and other payments to employees: Large companies need to pay salaries and other forms of benefits to employees at least once a month. Bulk salary payments simplify settlement with staff. They allow sending money to all personnel members simultaneously regardless of their number. Bulk payments also ensure that employees receive payments at the same time, contributing to the culture of equal opportunity. Payments to partners and suppliers: Businesses have multiple partners and suppliers whom they need to pay commissions on sales, bonuses for achieving goals, discounts for goods or services delivered, etc. Business partners are often located in different countries around the world, which adds complexity to transactions and delays payment times. Global mass payments simplify B2B transactions allowing companies to work in a more transparent and efficient way. Dividends to shareholders: Public companies must pay regular dividends to their shareholders. Considering that the law does not limit the number of shareholders, such companies can have literally hundreds of payees. Handling so many payments at a time can become a challenge. However, thanks to mass payment solutions, this challenge is easily solved, and companies can effortlessly send bulk payments to as many recipients as needed. E-commerce payments: E-commerce platforms make various types of payments. These include payments to vendors, affiliate commissions, referral rewards, promotional bonuses, and rewards to customers. Mass payout solutions make the settlement process fast and hassle-free. By processing payments in batches, businesses reduce the risk of errors and ensure that all recipients receive the required amount. Interest payments: Banks and other financial institutions regularly pay interest on long-term and short-term deposits. The number of recipients, in this case, can reach thousands of people. Batch processing payments provide great assistance for managing interest payment transactions. They help send the required amount to each recipient without delays or errors. Recurring payments: Mass payment platforms allow you to send and receive bulk payments. This is especially helpful for subscription services that regularly collect payments from a large number of customers. Mass payment management makes bulk transactions hassle-free. The whole process occurs automatically, and the company can be sure that the money goes to its account on time. How banks can enable mass payouts for clients securely and efficiently Banks and other organizations can enable bulk payments by choosing a reliable mass payment service provider (PSP). A partnership with a trustworthy PSP ensures payment security, transaction transparency, and technical support upon the client’s request. Typically, the process of activating business bulk payments through the mass payout platform occurs as follows: The company registers on the platform and tops up the balance in its personal account. Further, the deposited funds will be used to make mass payments. The company enters the details of the recipients to whom the money will be sent. It is not necessary to enter such details manually. You can, for example, download data from an Excel document. The company initiates a mass payment transaction. This initialization can take place manually or automatically. The payment service provider sends a request to the payment system via API. A request is also sent to the receiving banks so that they approve the money received. Once the transaction is approved, a mass payout is made. The money is debited from your account within the mass payment platform and credited to recipients’ bank accounts. A robust payment solution will also provide you with a detailed report on the completed transaction. It will save the history of previous transactions, allow you to view statistics for the selected period, and track data on mass payments over time. Top 10 benefits of bulk payments for banks By integrating mass payments, banks and other financial organizations open up the opportunity to make payments quickly and easily to any number of payees. Mass payments bring a lot of benefits to businesses. Here are just some of them: 1. Fast and hassle-free transactions By far, the biggest benefit of bulk payments is that they save you a ton of time. Imagine if you had to send 10, 100, or 1000 payments one after another. Processing such payments could take anywhere from several hours to weeks or even months. Bulk payments add all payments for processing into a bundle. Next, this bundle is processed at a time as a single payment. 2. Security and data protection Modern mass payout solutions use sophisticated tools and technologies to protect sensitive payment data. These include traditional tokenization and encryption, as well as blockchain technologies and decentralized ledgers.

How Faster Payments Empower Financial Inclusion in Banking

Categories How Faster Payments Empower Financial Inclusion in Banking All, Insights Under the influence of technology, organizations, and customers receive more advanced, convenient, and high-quality financial services. However, financial exclusion is the other side of the coin, which leaves certain social groups behind in the fintech ecosystem. The solution to this problem requires a comprehensive approach composed of social, economic, and, paradoxical as it sounds, technological measures. Instant digital payments are one such technological measure that allows financial organizations to expand their customer base and promote financial inclusion initiatives. The current state of financial inclusion in banking Fintech and financial inclusion are advancing rapidly. Just several years ago, many elements of modern banking that users actively use daily seemed like brand-new ideas. The world’s first ATM appeared in 1967. Today, there are about 3 million ATMs worldwide. In 1970, 51% of households in the USA had credit cards. Now, the percentage of US cardholders has reached 82%. In 1994, the first online payment was made. In 2022, the volume of digital payments reached $12.3 trillion, and it is expected to hit $20 trillion by 2027. Despite the expansion of financial technologies, many fintech services remain inaccessible to specific demographics. A look at global statistics demonstrates that global financial inclusion is uneven among countries and regions and may bypass certain age and social groups of society. Digital payments gained the most significant adoption in the Asia-Pacific region, followed by North America and Europe. These payments are least developed in Latin America and Middle East Africa. However, the growth trend of digital payments is observed across countries. It is expected that the global CAGR will reach 11.8% by 2028, with the volume of global digital payments solutions increasing from $112.2 billion in 2023 to $193.7 billion in 2028. Instant payment processing is leading in countries such as India, Brazil, China, Thailand, and South Korea. At the same time, instant payments in Europe and North America are slower, but these regions are on their way to establishing inclusive finance through a faster payment system. The most unbanked countries are Morocco, Vietnam, Egypt, Philippines, and Mexico, with the percentage of the unbanked population varying from 63 to 71% here. It’s worth noting that developed regions of the world are not the best examples of digital financial inclusion either. For instance, in the USA, 6% of adults were considered fully unbanked in 2022. This means that neither they nor their spouse or partner had a checking, savings, or cash account. The highest percentage of unbanking was observed among people with an income of less than $25,000 per year and in the age category of 18-29 years. Challenges of financial inclusion Access to financial services is crucial in overcoming poverty. The United Nations has identified financial inclusion as one of the key sustainable development goals. However, various challenges hinder global financial inclusion. Financial inclusion technology. Modern finance is increasingly dependent on technology. Digital real-time payments involve an internet connection, mobile or desktop devices, and behind-the-scenes mechanisms for data storage, transmission, and encryption. Considering that two-thirds of the population is unconnected, governments should focus on establishing widespread Internet connectivity, and fintechs should work on error-free transactions that are resistant to network interruptions. Financial inclusion cost. Technology comes with additional costs. After all, money is needed to create and maintain a payment infrastructure, and this money, as a rule, is collected from transaction participants in the form of commissions. Governments and investors should support fintech companies with additional cash injections to encourage consumers to use fintech services. Fintech companies, in turn, should look for more affordable instant payment methods, using innovative technologies and reducing fees. Cybersecurity and data protection. The digitization of financial transactions leads to new types of financial fraud. Cybercriminals use technologically advanced and sophisticated methods to gain access to payment data. This necessitates financial institutions to implement more thorough checks on customers before providing them with financial services. Consequently, some customers may be unfairly denied financial services. In light of this, fintech companies must develop Know Your Customer (KYC) procedures that provide a complete picture of potential clients. Such procedures must not only conduct a detailed check but also be bias-free. Artificial intelligence (AI) and machine learning (ML) are now increasingly utilized for such systems. Banks seeking to establish secure instant payments should partner with payment service providers (PSPs) that have advanced cybersecurity and KYC measures in place. How instant payment can promote inclusive finance Instant payments are a powerful tool for financial inclusion due to their innovation and customer orientation. Implementing instant payments benefits both businesses and customers because it involves more social groups in the financial ecosystem, offering more convenient and accessible financial services. Creating a faster payment system is not done overnight; it is a step-by-step process that requires effort from public banking institutions and fintechs. However, countries are gradually progressing toward creating an effective instant payment infrastructure, enabling instant payment for a broader range of consumers worldwide. Instant payments were invented to make payments immediately, that is, at the moment the transaction is executed. Unlike other types of transactions, instant payments do not have a delay in debiting money from the payer’s account and crediting it to the payee’s account. This immediacy allows real-time payments to attract and retain customers while promoting financial accessibility. The following benefits of real time payments make them a powerful tool for creating fintech financial inclusion. Benefits of real time payments for customers Control over the account balance. For many years, cash and cheques were the dominant payment methods. Even now, the number of cheque transactions remains relatively high. Users often chose cheques because they seemed safer than electronic payments, especially for expensive purchases. At the same time, the problem with cheques was the lengthy period needed to debit money from the payer’s account; sometimes, it could take up to 5 days. This situation made it impossible for the user to have up-to-date information about the account balance and prevented the ability to plan future

The Rise of Blockchain Payments: Cryptocurrency and Beyond

Categories The Rise of Blockchain Payments: Cryptocurrency and Beyond All, Insights Fast and reliable financial transactions play a pivotal role in efficient business operations. Technological advancements have opened new opportunities to optimize payment processing. One such advancement is blockchain technology. Blockchain payments are faster, more cost-efficient, and more transparent than conventional digital payments. Additionally, blockchain payments are known as highly secure, with a minimum risk of payment data leakage. Blockchain payment processing is increasingly used by businesses worldwide. The blockchain market is projected to reach $94bn by 2027, which is almost 13 times more than in 2022. Banking and financial services, retail and e-commerce, and government organizations emerge as the main blockchain users. It is obvious that blockchain technology is in a strong position within the fintech market. This article explains how blockchain payment works and how it can be applied in business. What is blockchain? Blockchain is a decentralized data storage based on a subsequent chain of blocks. Each block contains a certain portion of data and hashes from the previous block. This means that the data in each block is cryptographically linked with the data in the preceding block. Changes made in any blockchain block require recalculating the hash in that block. This, in turn, requires recalculating the hash in the next block and so on down the chain. Thus, a change in one block leads to changes in all blocks of the blockchain. Those blocks are located on multiple machines worldwide. Meanwhile, massive computing resources are needed to recalculate hashes and change data in each block. Given that, it is almost impossible to change data in the network. There are two types of blockchain: public blockchain and private blockchain. Public blockchain is available to anyone. This means that any user who wants to become a participant of the chain can do so. Private blockchain is available to a limited number of participants. Special permission is required to get into such a chain. Blockchain vs. cryptocurrency The notions of blockchain and cryptocurrency are often used interchangeably, but this is fundamentally wrong. Even though blockchain and crypto have common features, they are distinct concepts. The main difference between blockchain and cryptocurrency is that the former provides the technology for data recording, while the latter utilizes this technology to run decentralized transactions. In essence, cryptocurrency is a digital currency used in a decentralized network of users. It is called crypto because it utilizes cryptography methods to check transactions and create new cryptographic units. Cryptocurrency serves transactions that run on a public digital ledger, which is blockchain. The transaction data is stored on specialized computers within the ledger. Crypto transactions occur directly between transaction participants without intermediaries, such as banks. To clarify the blockchain vs. cryptocurrency difference, think of blockchain as an infrastructure that enables a specific way of data recording; at the same time, think of cryptocurrency as an application built on top of this infrastructure. Such an application would use blockchain capabilities to run monetary transactions in a new, more secure way. What do blockchain payments mean? Blockchain payments mean payment transactions executed with the help of blockchain technology. This includes blockchain cross-border payments, domestic payments, remittances, P2P transfers, etc. Notably, blockchain transactions do not necessarily rely on cryptocurrency. Traditional national currencies, such as the US dollar or Euro, can be utilized in blockchain money transfers. The main difference between blockchain payments and traditional payments is that the former uses digital currencies and no intermediaries, while the latter involves central financial authorities. The decentralized nature of blockchain payment solutions makes monetary transactions more secure and less expensive for businesses. That is why companies are increasingly adopting them to streamline operations and reduce costs. How blockchain payment systems work Blockchain payment systems work based on a chain of connected blocks containing transaction information. The new block is added to the chain when a new transaction is initiated. Payment processing using blockchain occurs in four steps: Step 1 The money sender requests to perform a transaction. They specify the sum to be transferred and the recipient’s details. Step 2 Transaction validators (miners) check if the sender has sufficient funds and confirm the transaction. Step 3 Once the transaction is confirmed, a new block is created and added to the chain. Step 4 The sent funds are deducted from the sender’s account and added to the recipient’s account. Once the transaction is confirmed, it cannot be canceled. Information about the transaction is recorded in all the subsequent blocks. This prevents the risk of changing it by cybercriminals. How businesses can enable blockchain in payment processing Businesses that want to integrate blockchain payment technology simply need to select a blockchain-based payment gateway or blockchain payment processor. Typically, a blockchain-based payment provider configures blockchain transactions, so no effort is required from the client side. Once everything is set up, the company can process blockchain payments similarly to how it processes traditional digital payments. Below is a typical flow of cross-border payments using blockchain used by banks: The customer A creates a payment of $500 from their bank in the US to customer B’s bank in Spain Once customer A’s bank approves the transaction, the sum is deducted from the customer’s account The deducted sum is sent to the bank’s pool account and is converted into the cryptocurrency of your choice The sum in cryptocurrency is then sent to the blockchain payment network you connected and converted into Euro The sum in Euro is credited to customer B’s bank account in Spain What challenges can blockchain payments solve? 81% of businesses believe blockchain technology is easily scalable and admit it is widely used in various areas. Mass adoption of blockchain in finance is not surprising because it solves different challenges for businesses, including the following: Dependency on centralized financial institutions. Blockchain payments occur in a decentralized ledger, which the transaction participants control. No intermediaries are involved in the transaction processing, and no lengthy approval procedures are needed. Transaction security. Payment information is the prime

Scan to Pay: The Ultimate Guide to QR Code Payment

Categories Scan to Pay: The Ultimate Guide to QR Code Payment All, Insights The rise of digital payments has dramatically changed the way transactions are made. Today, customers only need a smartphone to make a purchase in a store or send money to a friend. Quick Response (QR) code payment or Scan to Pay is a smartphone-only payment method that is gaining momentum. Businesses and customers love it for its fantastic convenience, high speed, and seamless transaction process. Today, this payment method is used in different areas, from e-commerce to bill settlement. The global QR code payments market reached $11.2 billion in 2022 and is predicted to hit $51.58 billion by 2032, showing a staggering CAGR of 16.5%. Thus, it is obvious that various businesses and monetary operations will increase their adoption of Scan & Pay in the coming years. Understanding QR code payment QR code payment is a non-cash, contactless payment method that allows users to make purchases by scanning the QR code using their smartphone. QR code payment is also called Scan to Pay, essentially because of the payment process: the user must scan a QR code to pay for goods or services. The QR code usually encrypts merchant bank details and information about a specific purchase. The seller shows the QR code to the buyer in electronic or printed form, and the buyer scans the code using a camera. After this, the purchase amount is debited from the buyer’s account and credited to the seller’s account within a few seconds. How does QR code payment work? Contactless payments with QR codes can be easily set up in online and offline stores or service centers. Here is how merchant QR code payment works: The seller creates a payment and generates a QR code. This is usually done in a particular QR code system. The seller can save the generated code as a picture in an electronic format or print it out for purchases in brick-and-mortar stores. The seller provides the customer with the generated QR code. They can do this by placing the QR code on the e-commerce website or brick-and-mortar store, in person, or by sending via email or messenger. The buyer points the smartphone camera at the QR code and receives a link with payment details. The buyer may then choose the preferred payment method, for example, credit card, Google or Apple Pay, or payment in installments. The buyer confirms the payment and sees a notification about the successful transaction. The seller receives the money in their bank account within seconds. The seller can also track the payment using their account in a payment QR code platform. How to set up a QR code for payment Merchants need to take three simple steps to enable Scan to Pay in their online or offline store. Here is how to set up a QR code for payment: Step 1. Choose a payment service provider. You need to research and select a payment service provider (PSP) offering a QR code payment option. Such providers usually charge a fixed fee or a percentage for each transaction. Make sure their pricing aligns with your budget. Step 2. Sign in to the QR payment system and select QR code payment. Your PSP will likely provide different payment options, such as credit card or mobile wallet payments. You need to set up your payment method for Scan to Pay and link it with your bank account details. Step 3. Generate QR code and present it to customers. Now that everything is set up and ready for accepting payments, all you need to do is generate the QR code and use it to complete the transaction. This procedure is usually completed in a couple of clicks and does not take longer than a few seconds. Top 7 benefits of QR code payments Scan and Pay technology provides businesses and customers with many benefits, including: Convenience. QR code is a fast and convenient instrument for payments. The seller generates the required code in a matter of seconds, and the buyer pays with a couple of taps on their smartphone. The transaction is processed instantly. Both seller and buyer receive notification of the transaction status. Versatility. QR code payments are successfully used by companies of different sizes and domains, including those that do not yet have a website or a physical store. Scan and Pay works great for sales through social networks or messengers, as well as in the traditional way. Cost-effectiveness. Scan to Pay eliminates the need to purchase a POS terminal and reduces fees associated with conventional payment transactions. Of course, Scan to Pay and QR code cannot fully replace other payment methods. However, this cost-effective alternative allows emerging businesses to quickly start with digital payments and established companies to expand their payment acceptance assortment. Reliability. QR codes are designed in such a way that even if part of the code is damaged or hidden, the transaction will still be processed. This is especially important for physical stores where QR codes are often printed. As a merchant, you can count on minimal to zero disruptions during the payment transaction. Speed. Scan to Pay is one of the fastest payment methods. After scanning the code, the funds are instantly transferred from the buyer’s account to the seller’s account. Thanks to high speed and convenience, the number of successful transactions and payment conversions increases. Global presence. Scan and Pay is used all over the world. By accepting QR payments in your store, you provide a familiar and convenient payment experience to customers. This payment method can potentially expand your customer base and increase sales. Customer care. The customer only needs a smartphone to pay for goods or services via a QR code. No cash, bank cards, or wallets are required. This is an ideal form of mobile payment for a modern shopper. By providing it, you demonstrate customer focus and commitment to current tech trends. Disadvantages of a QR code payment method Despite all the

Recurring Payments 101: Seamless Transactions for Powerful Businesses

Categories Recurring Payments 101: Seamless Transactions for Powerful Businesses All, Insights As financial technologies evolve, businesses gain new opportunities to ensure a smoother and faster payment experience for their customers. Today, fintech makes it possible not only to accept payments online but to differentiate the method of collecting funds depending on the type of transaction. Traditional one-time payments are unsuitable for businesses operating on a subscription basis. However, recurring payments are their way to go since they allow for regular charging of funds from the customer accounts. Consequently, it is no surprise that in 2023, the recurring payments market reached $13.2 trillion. By 2027, these numbers are expected to hit $15.4 trillion, demonstrating a staggering CAGR of 17%. Does that sound interesting? Continue reading to learn more and answer the most common questions, including “What does recurring payment mean, and how can your business benefit?” What is a recurring payment? Recurring payment is a regular payment method performed without the payer’s direct participation. With recurring payments, the customer does not need to enter a card number or company details every time they want to pay for a product or service. Instead, they fill out payment details once and agree to debit the money. When the payment deadline arrives, the money is debited automatically. The customer does not even need to confirm the transaction. Everything happens without their participation. The meaning of recurring payments for customers and businesses cannot be exaggerated. They provide an effortless payment experience and increase customer retention. What is especially important is that the recurring payment is highly secure. Even though the transaction occurs without the payer’s participation, it is reliably protected from fraud. How do recurring payments work? Recurring payments work thanks to special software provided by third parties involved in recurring payment processing. So, we have already found out what recurring payments are; now it’s time to see how recurring payments work and how to set them up. The essential steps are listed below: Transaction initiation. A customer who wants to buy a service or product enters payment details on the website or mobile app of the service provider or merchant. Before confirming payment, the buyer usually needs to check the Agree to Terms box. These terms clearly state the date and amount of payment and the fact that the buyer can cancel the subscription at any time. Payment data collection. The entered card details go to a payment gateway or PCI DSS-compliant payment service provider (PSP). The payment gateway or PSP converts the card details into a token and returns the token to the seller (in such a manner that the seller does not have access to the actual payment data). The token allows the seller to securely debit funds from the buyer’s card without the buyer’s confirmation. Transaction processing and confirmation. The payment gateway invokes the payment process at the defined time (once a week/month/quarter/year/etc.). It requests the issuing bank to confirm the debiting of the specific sum from the customer’s account. After confirmation, the money is debited from the buyer’s account and credited to the seller’s account. Both buyer and seller receive notification about the successful transaction. The case with failed transaction handling If there is not enough money in the customer’s account, the payment will not be executed. The customer will receive a notification that the transaction has failed and an explanation of why. The payment gateway will attempt to re-execute the transaction at specified intervals. The transaction will be processed successfully as soon as the money appears in the account. There are situations when a customer reissues a card and their payment information changes. You have nothing to worry about if your PSP supports the automatic card update. The funds will be debited from the buyer’s account and credited to your account with zero effort on your part. The automatic card update ensures that old payment details are replaced with new payment details automatically. Two types of recurring payments There are two main types of recurring bill payments: fixed and variable: Fixed recurring payments mean customers are always charged the same amount at the defined time. Fixed payments are usually recurring monthly payments or recurring annual payments. They are the most common type of regular payments used by businesses across domains. Examples of fixed online recurring payments are subscriptions to streaming services, memberships in sports clubs, and subscriptions to SaaS platforms. Variable recurring payments mean that the charged amount changes depending on the consumption. Variable recurring payments may also be less dependent on a specific period. This is especially true in a pay-as-you-go model, where customers pay for used resources. Examples of variable recurring payments are utility bill payments, cloud service payments, and Internet consumption payments. Recurring payment use cases in business There are a variety of businesses that accept recurring payments. The most common use cases are listed below: Subscription services: media with paid content, streaming platforms (music and video), radio station aggregators, cloud storages, file sharing services, and online TV. Membership organizations: gyms, fitness clubs, board game clubs, country clubs, and professional associations. SaaS providers: collaboration, task management, resource planning, customer support, marketing, and sales management platforms. Utilities: electricity, water, and gas companies and telecommunication providers. Insurance companies: they accept recurring payments from policyholders. E-commerce businesses: some platforms charge regular payments and, in turn, provide free shipping or exclusive offers. Online education platforms: with a recurring monthly payment, users gain unlimited access to educational videos, books, podcasts, etc. Software maintenance: users with premium subscriptions may count on instant responses and 24/7 support. Benefits of recurring payments for SME What is a recurring payment for a small business? This is primarily a way to retain customers and grow income. After all, users who subscribe to your website or app will regularly pay you money, even if they forget the payment date. On top of that, the recurring payment meaning for small enterprises is further enhanced due to the following benefits: Reduced number of purchase refusals. The customer makes

The Why’s and How’s of Payment Tokenization

Categories The Why’s and How’s of Payment Tokenization All, Insights Digital payments initially aim to improve user experiences, accelerate business cash flows, and optimize operational costs. However, this is in theory, while in practice, electronic payment transactions face multiple hurdles preventing those benefits. Additionally, risks related to attackers’ ability to gain access to the customer’s payment data are another problem of electronic payment transactions. If this happens, the customer will lose their money, and the company processing the payment will lose the customer. Given this, protecting sensitive financial information is crucial for businesses involved in payment transactions. One of the best methods to address those challenges is payment tokenization. This article will answer the main question: what is tokenization in payments? Plus, we will consider how tokenization works and how businesses can benefit from it. The next level of payment protection: tokenization payment meaning First things first: what is payment tokenization? Tokenization replaces vulnerable card payment data with a unique set of characters called a token. Essentially, it is a type of encryption. The token can be transferred between software systems and used for transactions without disclosing sensitive data. Even if someone gains access to the token, they cannot use it since it does not contain real payment information. The data, being tokenized during the payment transaction process, is typically as follows: Card number Owner’s name Expiration date Bank account number Tokenization is one of the most reliable ways to protect data. It securely hides payment card details, preventing criminals from accessing it and causing fraud. Payment tokenization vs. RWA tokenization Tokenization technology is used not only in online payments but also in other business areas. It can be used to protect personal data and user rights to possession of assets. Given this, it is necessary to distinguish the concepts of online payment tokenization and RWA (real-world assets) tokenization. Tokenization of real-world assets means digitization of actual assets. The latter is represented in the form of digital tokens in distributed ledgers, blockchains, and other asset tokenization platforms. The assets can be the objects of real estate, art, commercial enterprises, luxury goods, etc. Each token represents a fractional ownership of the specific asset. This provides greater liquidity and accessibility to a broader range of investors. Thus, tokenization is used in payment transactions to encrypt and protect payment card data. In asset management, it is used to fix rights to assets and simplify the investment process. Although payment tokenization and RWA tokenization have similarities, they are different concepts that should not be used interchangeably. How does payment tokenization work? Imagine that you are making a purchase in an online store. To pay for a product or service, you need to enter your card details on the store’s website. If such a site cooperates with a payment provider that supports payment tokenisation, you have nothing to worry about because your data is reliably protected. However, if card tokenization is unavailable, there is a risk that third parties will access your payment data. Below, we will analyze how tokenization in payments works: A customer enters card details into the payment gateway on the merchant’s website. The payment gateway redirects the payment card data to the payment provider. The payment provider converts the card data into a token. The payment provider returns the generated token to the merchant and creates a reference of this token with real payment data on its side. The merchant’s payment gateway requests that the payment system generate a network token. The system requests permission to generate the network token from the bank that issued the customer’s card. The issuing bank verifies the request for payment network tokenization and returns a response along with the actual payment data. A unique network token is generated and linked with actual payment data. When a merchant needs to withdraw money from a card associated with a specific token, they send a request to the payment provider. The payment provider matches its token and the network token. At this moment, the network requests permission from the issuing bank. When the issuing bank gives a positive response, the money is debited from the customer’s card using the token. Top 5 benefits of tokenization in payments Fintech is the driving force behind the development of the financial sector. Modern fintech companies are actively introducing new products to the financial market and breathing new life into traditional financial transactions, including cross-border payments. Thanks to fintech companies, consumers get a new experience of sending and receiving money and tangible benefits of cross-border operations, such as: Security The token itself is of no value to criminals because it does not contain a card number or other details that can be used when making a transaction. Acting as a cipher, the token is simply a collection of useless symbols to whoever gets their hands on it. Decrypting the token and retrieving the original card data from it is hardly possible. Confidentiality In a scenario where an attacker obtains card data, they, among other things, gain access to the username. This can be further used for malicious purposes, from falsifying information to robbery and other criminal scenarios. Tokenization of credit card transactions protects users’ personal data and maintains their confidentiality. Convenience Tokens can be reused to make payments. That is, having made a payment once, the user can check the box to save the card for future payments. At this moment, the token will be saved, not the actual card number. However, the customer will not need to re-enter payment information for future purchases. Fast processing The tokens themselves are shorter and lighter than the card number and associated user information. This allows you to send and verify them faster. As a result, tokenization payment processing is more streamlined and efficient than card data processing in the original way. Compliance Payment Card Industry Data Security Standard (PCI DSS) recognizes payment card tokenization as an effective measure to ensure payment security. Therefore, by tokenizing online transactions, you can quickly get closer to

Cross-Border Payments: How Fintech is Making Them Faster and Cheaper

Categories Cross-Border Payments: How Fintech is Making Them Faster and Cheaper All, Insights In today’s connected world, businesses and people are increasingly using cross-border payments. Such payments enhance global commerce and improve the consumer experience. As for non-commercial P2P operations, they allow people to be more in touch with relatives and friends and open a wider field for activities in various life situations. However, traditional ways of sending money abroad are often slow and expensive. Financial technologies take overseas payments to a new level, making them more accessible, simple, and secure. Challenges with traditional cross-border payments Traditional cross-border transactions often involve several intermediary or correspondent banks. This has a direct impact on how payments are processed and creates specific challenges for international payment processing, including the following: Regulatory compliance. Correspondent banks and international payments undergo strict regulatory procedures. These include but are not limited to, anti-money laundering (AML), know your customer (KYC), anti-fraud, and data protection regulations. While these procedures are essential for protecting data and funds, they often slow down the transaction and make it less flexible. High fees. Each correspondent bank charges a fee for participating in a cross-border money transfer. In addition, transaction participants may incur significant fees for currency conversion, wire transfer, and other operations associated with traditional cross-border remittances. This makes cross-border banking unaffordable for most customers and encourages them to look for alternative cross-border digital payments. Long processing time. Traditional cross-border payment process flow may exceed three business days. This is because the transaction goes through multiple third parties and regulations. Such a long period may be unacceptable for businesses that need fast funds availability for subsequent operations. It also doesn’t meet the needs of P2P payments, where customers want to send and receive money quickly. Insufficient transparency. Traditional international payment has a complex structure, which complicates its visibility. Parties do not always know the status of a transaction. They may also receive delayed updates when a transaction fails and miss the opportunity to fix it. Such a situation negatively impacts businesses because responsible persons cannot make informed decisions based on real-time insights. Lack of innovation. Traditional banks often have legacy IT infrastructure and processes. They depend on state authorities, which restricts their flexibility in making innovative decisions. Lack of innovation makes monetary operations less efficient and compatible with the modern digital world. It prevents banks from meeting user expectations of what cross-border payments are to be. Changes in the world of cross-border payments Global businesses cannot survive without crossborder payments. As competition and customer demands grow, they need more instant, reliable operations that can be executed hassle-free. In recent years, cross border financial transfers have transformed significantly due to technological progress. One of the main technological endeavors is Swift’s Global Payments Initiative (GPI). Since its introduction in 2017, GPI has dramatically changed the landscape of international payment methods. Its main advantage lies in the high speed of overseas transactions and extensive geographical reach. With GPI, anyone anywhere in the world can receive or send money. Another big step in improving cross-border payments is the roll-out of the ISO 20022 standard. ISO 20022 classifies financial data and translates it into a common language for people and machines. For international payment operations, it means enhanced data interoperability and seamless transaction processing. Starting in 2025, any institution that sends or receives mobile terminated (MT) payment-related messages via Swift will begin using ISO 20022. Distributed ledger technologies (DLT) are changing the technological context of international settlements. If previously cross-border transactions were mainly centralized and regulated by central banking institutions, now they are gaining autonomy and self-regulation. Distributed ledgers provide great transparency to the participants in the transaction. It also reduces the risk of fraud and the cost of international payments. Application programming interface (API) is a modern facilitator of cross-border payments. Thanks to the use of APIs, payment ecosystem applications easily communicate and instantly transfer data from one payment service to another. APIs also contribute to better security of banking software systems and reduce manual work. You can use API to make bulk payments, among other things. This can be useful when, for example, you need to make payroll to the staff abroad. Last but not least, the technology on our list is central bank digital currency (CBDC). As the name suggests, this currency is issued by a central bank of a specific country. Unlike traditional currency, CBDC runs on the distributed ledger platform, which means any intermediaries in the transaction process are removed. Thanks to its distributed nature, CBDC has enormous potential to reduce the cost and time of cross border payments, making them near real-time. Currently, 130 countries are looking to develop their own CBDCs. The role of fintech in cross border payments Fintech is the driving force behind the development of the financial sector. Modern fintech companies are actively introducing new products to the financial market and breathing new life into traditional financial transactions, including cross-border payments. Thanks to fintech companies, consumers get a new experience of sending and receiving money and tangible benefits of cross-border operations, such as: Lower costs Fintech companies omit many intermediaries involved in the traditional banking system. This allows them to avoid additional fees and reduce the transaction cost. Higher speed Fewer intermediaries also mean a higher speed of cross-border payments. In addition, fintechs are constantly looking for new ways to optimize their operations to attract and retain more customers. Smoother UX Fintech reduces bureaucratic procedures associated with cross-border payments. It ensures that the user spends minimum effort creating a transaction via a cross border payment platform and receives approval within seconds. Better control Parties can monitor the status of transactions in real time. They also have greater confidence that it will pass successfully due to its non-centralized nature. Greater agility Fintech companies are flexible in choosing cross border payment technologies. They can quickly optimize operations according to user and market demands. Top 5 cross-border payment methods The following methods are now dominating the cross-border payment market: Cards.

The Rise of Paytech and Its Impact on E-Commerce

The modern business world is fast. Companies are looking for every possible way to speed up deals, reduce delivery times, and minimize operations downtime. Enabling real-time payments (RTP) is crucial for ambitious businesses. RTP payments contribute to bigger sales and provide superior experience to customers. In many countries, real time payments are already widely adopted. However, there is still much room for RTP development, both from geographic and technological perspectives.

Going Fast or Last: What Are Real Time Payments?

The modern business world is fast. Companies are looking for every possible way to speed up deals, reduce delivery times, and minimize operations downtime. Enabling real-time payments (RTP) is crucial for ambitious businesses. RTP payments contribute to bigger sales and provide superior experience to customers. In many countries, real time payments are already widely adopted. However, there is still much room for RTP development, both from geographic and technological perspectives.

Top 6 Challenges of Digital Transformation in Banking

Digitalization remains one of the hottest topics since the pandemic outbreak. While many blame businesses for being sluggish, few understand what actually holds them back. Digital banking transformations are no exception, and about 63% of bank leaders believe that they have failed to win new consumers due to slow transformation, according to the 10x Banking report.

Fintech Revolution as a Logical Response to Slow Banking Digital Transformation

Over the past five years, tech advancements and customer demand have moved the fintech players from the fridges into the mainstream. Admittedly, this growth was explosive, as it was energized by regulators, massive investments, customer favor, and stagnation in the banking industry.

DCM Joins the Independent Association of Banks of Ukraine as Associate Member

DCM, an innovative software vendor, partners with the Independent Association of Banks of Ukraine to drive payment innovations, accelerate transactions, and improve customer experience.

Tokenized Deposits for Merchants

In today’s fast-paced business landscape, the need for swift and cost-effective payment solutions has never been more crucial. Enter Tokenized Deposits, a game-changing innovation that promises to change how merchants receive payments. This groundbreaking approach offers lots of advantages, from near-instant fund accessibility to eliminating commission fees, all while ensuring top-notch security for both merchants and clients.

DCM’s solution is to leverage the distributed ledger network solutions on behalf of the group, focusing on payments for businesses and tokenization for customers.

Pricing in real-time payments

Real-time payments are spreading rapidly around the world. The economics of retail payments are proving to be more complex. Traditionally, the financial models for card payments have included merchant fees and their distribution among participating financial institutions (interchange). However, the approach to pricing for instant payments is significantly different. Markets and regulators are revisiting the main scenarios, phasing out interchange (e.g., in Brazil and Singapore), imposing limits (in Jordan), or even eliminating fees (in India and Mexico).

Open Banking: A Catalyst for the Emergence of Embedded Finance

Open banking initiatives have been launched in various economies worldwide. Built on the foundation of providing open access to banking data for the more significant benefit of customer choice, open banking presents numerous challenges, with security being an important concern.